Most experts consider homeownership as the best engine to create long-term wealth.

“A study of the old feudal land system of England provides us with an invaluable glimpse of legal history regulating the most valuable asset of them all: land. In medieval times, the land was the only form of wealth.”—A Brief History of Real Estate Law

Today, housing is the most valuable financial asset among American families. Owning a home is the cornerstone of the American Dream. Homeownership combines emotional, financial, and community bonds into a single transaction.

While homeownership is the basis for the political and social development of neighborhoods and communities, it is also the time-tested vehicle to build the wealth that sustains the property owners and heirs well into the future.

Researching, evaluating, and buying a residence is also one of the most complex financial transactions most people will enter into in their entire lives.

The financing process requires the formal, in-depth financial verification of the property’s owners. It is usually accompanied by a complete legal description and proof of the real estate asset. It involves local, county, and state tax and building authorities.

The Real Estate Factor

English Common Law in 1066 AD regarded real estate as the only form of wealth. When the Norman king, William the Conqueror, occupied Great Britain in 1066, he took possession of all the land. He then granted temporary use of the land through a system called “tenure” to his followers.

With access to the king’s land, people who had tenure could hire local inhabitants to work the land in exchange for rent, goods, or services. With property and the buildings on the land at its core, this became the feudal system’s foundation.

Since the king owned the land and granted access to it by special dispensation, real estate evolved as formal transactions. Land and property ownership carried special rights to political, financial, and social rank. It allowed landowners to charge rent and build businesses based on agricultural, light industry, craft, and livestock production.

These special rights gave tenure holders economic and political power backed by the evolving special provisions of English Common Law related to property use and property rights.

Real Estate ownership in the U.S. has its foundation in English legal theory and case law. It has special status of real estate property ownership, relationships with mortgage firms, and local development and taxing authorities.

Building Wealth by Homeownership

With all this as a backdrop, this article addresses how real estate and homeownership, in all of its varied forms, should be considered the best wealth-building engine that is available to average Americans.

While homeownership spans from basic shelter, condos and luxury homes, they have common financial traits that deliver benefits.

Ownership also changes over time as its owner’s age, retire, die, or become ill. At each significant stage in this human lifecycle, the benefits and obligations of ownership become evident and accessible.

It is also important to note that real estate ownership in all forms carries both the pros and cons of assets and liabilities. Real estate ownership, in most forms, requires insurance, taxes, maintenance, depreciation and repairs, replacement, and inspections.

While it means expenses for homeowners, it also points them to benefits associated to their ownership.

This article will look at homeownership, what it offers, and its financial benefits as the best engine to create wealth.

Housing as a Financial Asset and Liability

A financial analysis lists financial and non-financial assets.

Financial assets include:

- Stock

- Bonds

- Cash accounts

- Mutual funds

- Insurance

- All types of liquid investments held in bank, brokerage, and retirement accounts.

Non-financial assets:

- Less liquid or assets that are not readily and quickly convertible to cash, like houses or other large properties.

Housing accounts for about 70% of the assets of middle-income Americans age 55-64, excluding the value of Social Security and defined benefit plan pensions. Among retirees, housing is typically the largest overall item of expense for retirees.

On the liability side, housing expenses generally constitute a significant share of total spending in buyer’s lifetime. One study found that housing expenses included 31% of all expenditures for all consumer units (presumably with retired and employed household members) and more than half of housing expenses for homeowners are for mortgage payments.

Numerous academic and government studies show that home equity has a paramount role in determining overall household wealth. A 2011 study by the U.S. Federal Reserve found that housing wealth accounts for about 50% of total household net worth ($52.9 trillion) and is larger than the Gross Domestic Product ($14.4 trillion). This same study also cited the link between housing wealth and spending patterns. From 1952 to 2008, the correlation between housing wealth and personal consumption spending “tend to move together.”

Housing ownership also skews by age. People over age 55 have the highest percentage of homeownership. A 2004 survey of consumer finances found that Social Security accounted for 42% of total wealth for a typical family approaching retirement (sample household headed by a person aged 55 to 64), followed by the principal residence (21% of total wealth).

More recent data from the U.S. Census and other sources found that housing is the largest single financial asset among American families, especially among homeowners headed by the age group approaching retirement (usually age 55 – 64).

How Homeownership Builds Wealth

“There is nothing which so generally strikes the imagination of mankind and engages the affections of mankind as the right of property.”

—Judge William Blackstone, “Commentaries on the Laws of England, 1766

The dream of homeownership has been a persistent feature of American society since Thomas Jefferson promoted land ownership as an essential nation-building element. After World War II, ownership became more available and affordable through a combination of G.I. loans, the expansion of the Federal Housing Authority (with its low-down-payment policy), and dedicated residential suburban tracts.

As the middle class grew, the residential real estate industry continued to expand its residential product offerings. In the late 1970s, the residential mortgage industry began to develop a wider variety of loans. The key was different down payments, terms, and interest rate combinations to make homeownership more available to a broader audience.

Interest Rates, Homeownership and Price Scalation

Partnered with lower interest rates, it helped increase homeownership in the U.S. from 64% in 1995 to 69% in 2015. The peak in U.S. homeownership was 68.8% in 2005. This increase reversed a homeownership trend that was nearly flat for 30 years.

Chart Source: Seeking Alpha

As homeownership increased, real estate values began a gradual escalation, with median home prices rising from $18,000 in January 1953 to $301,000 in January 2020. From 2000 to 2005, the gap between median home values and median home incomes of households headed by people aged 30 to 34 increased in 49 states, most notably in the West.

Homeownership also builds wealth by accessing home equity value that builds over time. Equity is so critical because home equity comprises a large percentage of a retiree’s net worth. (Net worth is the value of all assets minus all debts.) The U.S. Census found that in 2017, 66% of the median net worth for householders of at least 65-years-old derived from their home equity. In 2017, the median home equity for people over age 65 was $170,000.

Homeowners can use their equity to do four things:

- Take out a home equity loan (known as a second mortgage)

- Obtain and borrow against a home equity line of credit (HELOC)

- Refinance their home with a larger mortgage and take the cash (a cash-out refinance)

- Obtain a reverse mortgage.

- Change their home for a cheaper one and cash out the exceeding money

All of these factors demonstrate the benefits of homeownership:

- Appreciation, accessing home equity, and reducing taxes on real estate-related activities.

- Homes have generally appreciated over time, especially compared to stocks and bonds.

- Homeowners build community relationships and have an emotional connection with their homes.

- Owners can earn “sweat equity” by making improvements in their homes and benefit from favorable tax treatment.

- Retirement funding through various tools, such as reverse mortgages, refinancing, and taking out a line of credit.

The Risks of Homeownership

However, homeownership is not entirely risk-free. Home prices fluctuate, and prices can vary significantly by location, even by zip codes. Home prices also are very susceptible to economic shocks, such as recessions and housing bubbles.

Most recently, the 2008 recession was precipitated by a housing bubble. In this last case, the housing recession wiped out almost $3.3 trillion in home equity. It caused a national economic shock wave that took some areas of the country a decade to recover.

Declines in home values also disproportionately impact Afro-Americans and Hispanics, who often have less secure jobs and whose homes may suffer more severe price declines than those in Caucasian neighborhoods.

Homeownership and Millennials

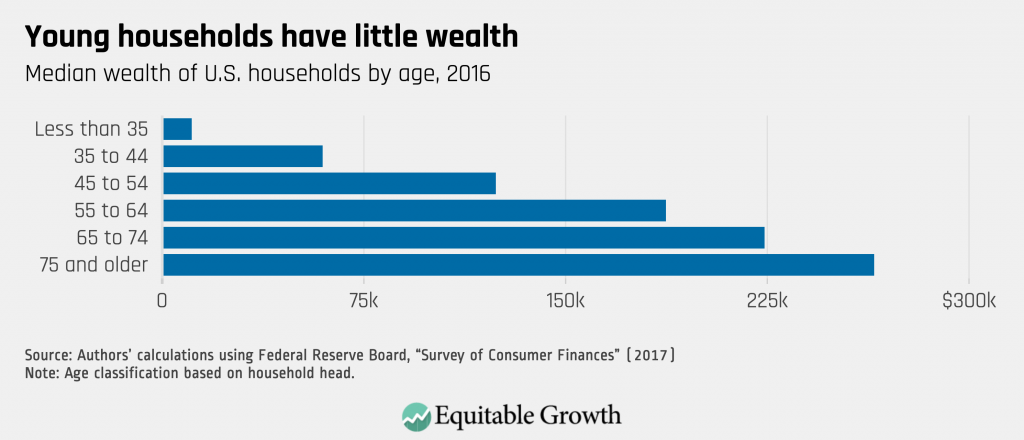

While this paper thus far has focused on how housing wealth is created, researchers have noted changes in first-time homeownership patterns as they affect wealth creation among younger people (under age 35).

One of the most significant changes is among first home buyers. New home buyers are slowly getting older. A report by the National Association of Home Builders found that first-time homebuyers’ median age rose to 33-years-old, the oldest in records dating back to 1981. The median age of all buyers was 47, a new record that was well above the median age of 31 in 1981.

New home buyers are older because real estate prices have also increased. While the median U.S. household income remained essentially flat in 2018 at $63,200, according to data released by the U.S. Census Bureau, new home buyers’ incomes have increased. According to a Bloomberg report, the typical income of new home buyers increased to $93,200 in 2018 mainly because a tight inventory of homes has pushed lower-income potential home buyers out of the market,

Lower Value to Income, but More Spending

Despite these income levels, beginning in the early-2000s, new home buyers could finance a house purchase with a significantly lower value-to-income ratio. A study found that for buyers to pay for these homes, they spent two times more of their after-tax income on mortgage servicing in 2005 versus 1976.

Due to innovations in the mortgage industry, including the development of a secondary mortgage market, relaxed credit requirements, securitization, and changes in Federal Reserve Board regulations (most noticeably Regulation Q), more people have been able to buy more expensive homes.

So, while homeownership continues to have emotional and financial significance, the trade-off between first-time buyers spending more of their after-tax income on mortgage servicing may mean less money is available for retirement savings.

This carries an implied bet that house prices will continue to appreciate at a rate exceeding other more liquid market investments, or at least, that the home will continue to serve as a primary source of future wealth creation.

Housing Wealth and Consumption Patterns

Both housing appreciation and depreciation affect consumption patterns of goods and leisure. Academics believe these patterns largely follow the Lifecycle Hypothesis, developed in the Fifties and Sixties, positing that income variations over a person’s lifetime are equalized by either borrowing or spending from existing wealth smooth out consumption levels.

In practice, younger people will borrow in anticipation of future incomes, while people in mid-life reduce spending to accumulate wealth to maintain a level spending pattern in old age. Other variables that affect the Lifecycle Hypothesis spending patterns are household ages, bequests, projected earnings, and life expectancy.

More recent studies and modeling of consumption patterns based on increased housing and stock market wealth found a greater propensity for consumer wealth to be generated from an increase in housing (in the range of 5% to 9%) versus gains from financial assets (2%).

One study found that households spend about 5% of every dollar in annual house price appreciation, and this spending level accelerated faster than gains from stock appreciation. The study believed that accessing house equity appreciation got easier through the greater variety of home equity loans.

Another critical result affecting housing patterns is that more seniors face the prospect of moving as they age. A 2018 AARP study found that 75% of people over age 50 and older want to stay in their homes and communities as they age; only 46% said they could remain in their current homes for various accessibility and mobility-related reasons. This means the desire to maintain a house for as long as possible makes retirees and pre-retirees more susceptible to house price declines and other related medical factors.

Tax Implications of Homeownership

Owning a home presents distinct tax advantages. Specifically, from saving on tax payments from deducting mortgage interest, property taxes, and financing costs. The most significant deduction often comes from making interest payments on either primary or secondary residences.

Another deduction comes from the points buyers pay at closing that reduce the interest rate on the mortgage. Often, these deductions are amortized over the entire term of the mortgage. For people who took out a line of credit or a home equity loan before 2018, that interest may be deductible if those funds were used to “buy, build or substantially improve” the borrower’s primary or home, according to the IRS Publication 530.

Other non-tax benefits of homeownership include greater financial flexibility due to secured borrowing, built-in “default” savings with mortgage amortization and nominally fixed payments, and the potential to lower home maintenance costs through sweat equity.

Housing Options Available for Retirees

Besides tax benefits, homeowners have access to equity loans and credit lines to access cash appreciation and home value.

Another option for securing home equity is an outright property sale. Many retirees, or people approaching retirement, downsize and move to a smaller house to cash-out their home equity. These proceeds can finance assisted living or skilled nursing care.

Planning to sell the house at a time of future need is risky in a world when home values fluctuate. Also, if the house is not well maintained, its value can decrease.

Retirees on Medicaid may also use their home equity to obtain long-term care services in retirement. Depending on the state, some states might attach home equity after the homeowner dies to recoup Medicaid expenses.

Housing Wealth, homeownership and its Effect on Key Retirement Decisions

While homeownership is the engine for creating wealth, it also produces strong sentimental and psychological effects. A study of retirees indicates that most have not tapped their home equity to pay for current living expenses, even though 70% of these homes are mortgage-free by people over age 65.

Their reasons for not accessing home equity varied. Some said they wanted to keep their house instead of selling and then paying rent. Older people who want to keep their homes also contradict the long-held lifecycle model of consumption, which found that older people consume more as they age.

However, despite the large amounts of potential home equity available to older Americans, over 55% said they would not take out a loan unless they suffered a financial, medical, or emergency event. Among the reasons, financial conservatism, older people working longer, and the desire to leave an inheritance to their children.

Home Equity and Vital Decisions

Owning a large amount of home equity also affects other vital decisions regarding work patterns for older Americans. These decisions include:

- Whether older people feel the need to work to meet monthly mortgage payments.

- Whether couples feel the need to work and own their house when they receive favorable treatment under Medicaid and similar benefit programs. In these instances, homeownership is not included in the asset limit test used by some states to determine eligibility for Medicaid or Supplemental Social Security.

One study found that homeownership, including the amount of home equity, affected the need of older women to continue working in old age. This decision to continue working was also highly dependent on marital status, wealth, and education. As a result, any decrease in house value, combined with the need to meet mortgage payments, could alter retirement plans.

These decisions to continue working in old age have a disproportionate impact on women due to their historically different labor force roles. Women traditionally have shorter or more interrupted work histories than men due to childbearing and rearing. They also earn lower wages and have a higher rate of participation as caregivers to aging parents.

This creates a more severe impact on women’s retirement security. It may also help explain why 30% of single women (who represent a majority of U.S. households in old age) fall into the category of poor or near-poor.7

The Role of Reverse Mortgages

Reverse mortgages allow homeowners to borrow against their home value without making monthly payments. The loan principal and interest are paid when either the house is sold, the last surviving spouse dies, or the borrower fails to meet the mortgage terms.

Unlike other home loan products, borrowers using a reverse mortgage do not pay monthly payments. It results in an escalating compounding interest that is added to the principal and must be paid annually. Owners of reverse mortgages must pay real estate taxes and any required flood and homeowner insurance premiums. When the reverse mortgage holder dies,

Reverse mortgages fall into two categories. The popular government-backed Home Equity Conversion Mortgage (HECM). Originated from private lenders and insured by the Federal Housing Administration (FHA).

The second and less popular, is a reverse mortgage issued by private lenders that is not federally insured.

HECMs are often used by people who have lower credit ratings. It is because they often have fewer resources to make regular monthly payments. They are less likely to be approved for other home loan products, such as equity lines of credit. When the borrower dies, can no longer live in the house, or it is sold, someone must pay in full. If there is any equity remaining, it can be transferred to the borrower’s heirs.

The Impact of Housing Shocks, Recessions and Recovery Scenarios

For Baby Boomers planning to retire, housing wealth accounts for a majority of total net worth. Home equity accounts for one-third of net worth at the mean and 50% median.

It makes Baby Boomers especially susceptible to housing price shocks, both positive and negative, significantly affecting retirement planning and consumption patterns.

When house prices drop due to economic shocks or housing bubbles, it has a compounding effect on diminishing household wealth. This produces a cascading effect that impacts entire families, primarily single or divorced women, and widows. The 2008 bear market caused workers aged 45 to 64 to delay retirement plans and borrow from their 401(k) accounts.

What if Your Home Price Falls?

The decrease in housing values is especially significant since homeownership increases with age. Older people rely more on home equity as a source of wealth and as insurance against unforeseen adverse life events. Decreased home values also have resulted in reduced confidence in future retirement planning for people of all ages.

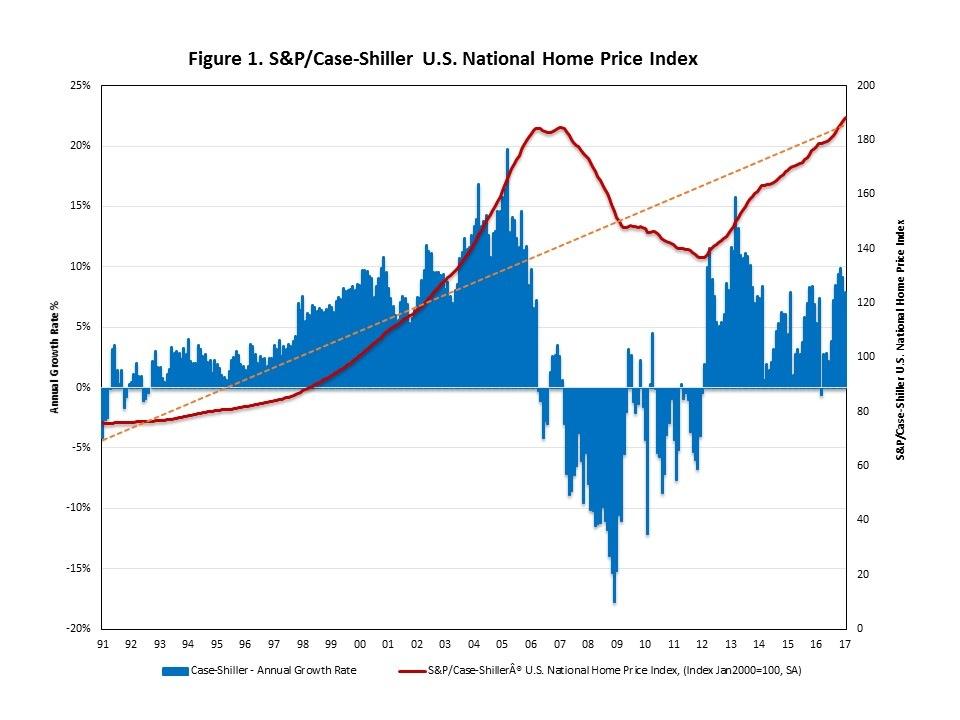

Housing prices are slow to appreciate and even slower to recover after a shock, as the following numbers illustrate. Using the Case and Shiller Index of U.S. national housing prices dating back to 1890, home prices hit an all-time high in 2006 Q1. In December 2008 (around the start of the housing bubble bust), the index posted its most significant year-to-year drop. After the housing bubble began around 1999, the index’s low point was in 1Q 2012, at 114. By 4Q 2013, the index had rebounded to 134.

And if the 2008 housing market crash and the resulting recession serve as examples, declines in house prices, combined with the over-supply of foreclosed and for-sale homes, created a ripple effect on the entire housing market. This 2008 market event caused the foreclosure of about eight million homes. It also destroyed about $7 trillion in home equity. One study found that housing market corrections have historic cycles lasting three to seven years.

Worse than just the Price Drop

But home price declines are only a part of the problem. As a result of the 2008 housing market bubble, new housing cycle corrections could take over 20 years to reach an equilibrium state where buyers and sellers are proportional.

The reason: When Baby Boomers aged 65 to 75 began to sell their houses after the 2008 housing crash, there were three sellers for every buyer.

This created a “generational housing bubble” on top of the speculative housing bubble developed from 2005 to 2007. This shift (more sellers than buyers) started around 2010. In the past, without this significant change in demographics, housing corrections historically lasted three to seven years.

Any new housing bubbles would differ on a state-by-state basis as the number of older homeowners declines relative to younger homebuyers. Still, its overall impact will be the same: there will be too many sellers to sustain house price increases. This situation also would profoundly affect suburban areas where there is a preponderance of stand-alone, single-family homes.

Finally, the 2020 COVID-19 pandemic added more uncertainty as employers adjusted their work behaviors.

The Impact of Homewnership Discrepancies by Race

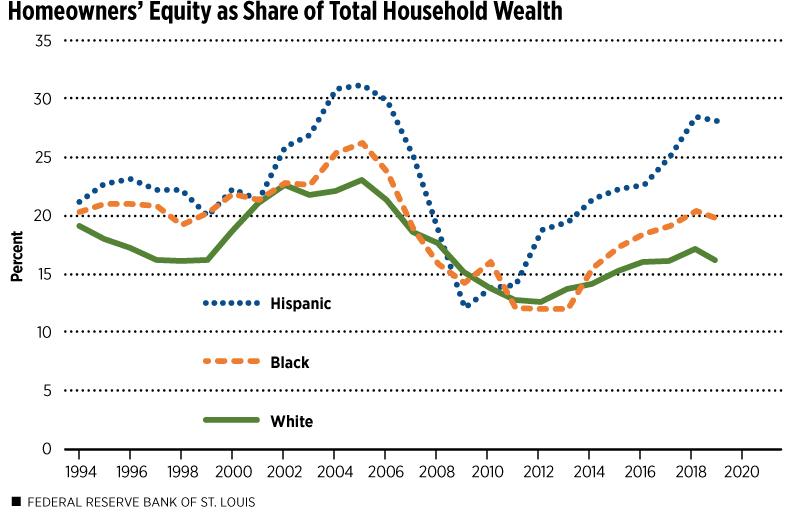

Due to the wealth discrepancies among different races in the U.S., it is not surprising that homeownership among Afro-Americans and Hispanics is significantly lower than among Caucasians. Over generations, this has contributed to the demonstrated pattern of wealth disparity among races that exists today.

As noted in the 2018 study, Homeownership and the American Dream, “homeownership rates for black households have fallen every decade for the last 30 years, both unconditionally and after controlling for income and demographics. Even in 2015, black households with a college education are less likely to own a home than white households whose head did not graduate from high school.”

Chart Source: Federal Reserve Bank of St. Louis

Homeownership rates for blacks have declined relative to whites and Asians. In 2015, the homeownership rate among Blacks was 42.2% and 45.4% for Hispanics compared to 70.8% for Caucasians.

Also, other studies have found that minority borrowers are more likely to become delinquent on their mortgage loans. Home prices at the lower end of the market are more volatile than homes with higher prices, exacerbating the size of wealth effects (positive and negative) for lower-income and minority borrowers with higher-than-average loan-to-value ratios.

Suburban locations with a high minority share of residents may also have lower appreciation rates than areas with a higher percentage of non-Hispanic white residents.

Wealth Creation is a Marathon Race, Not a Sprint

In this technology-driven world, speed is often the primary measure of success in evaluating business growth, product development, deployment, and market expansion. However, when it comes to building personal wealth, speed becomes a minor factor.

One reason for this shift is life factors, such as the human life cycle, demographics, and uncertainties in life. Wealth creation can be derailed by extraneous and personal characteristics, such as marriages, deaths, divorces, and births.

Similarly, buying a home requires years of savings and a severe search and evaluation process before the mortgage company hands the new owner the keys. The house can then take years to increase in value even as the markets go through its inevitable value cycles.

Overall, the effort of buying a house is worth the significant financial investment and emotional struggle. Good things take time to develop; wealth creation through homeownership is no exception.

–Chuck Epstein