First-time home buyer loans can be disturbing due to paperwork and the lack of widespread knowledge. However, these mortgages are actually some of the most powerful tools available to people looking to buy their first home. It’s not in vain that over 2 million houses are sold to first-time buyers every year.

Everyone dreams of owning a piece of land they can call home. In this article, you will learn everything you need to know about first-time home buyer loans, requirements, and even zero down payments.

Getting the best first-time home buyer loans is crucial, especially in 2022, a year expected to be the time frame in which the Federal Reserve is expected to increase three times its interest rates.

Do you want to know which loan will be best for you as a first-time home buyer?

What is a first-time home buyer loan?

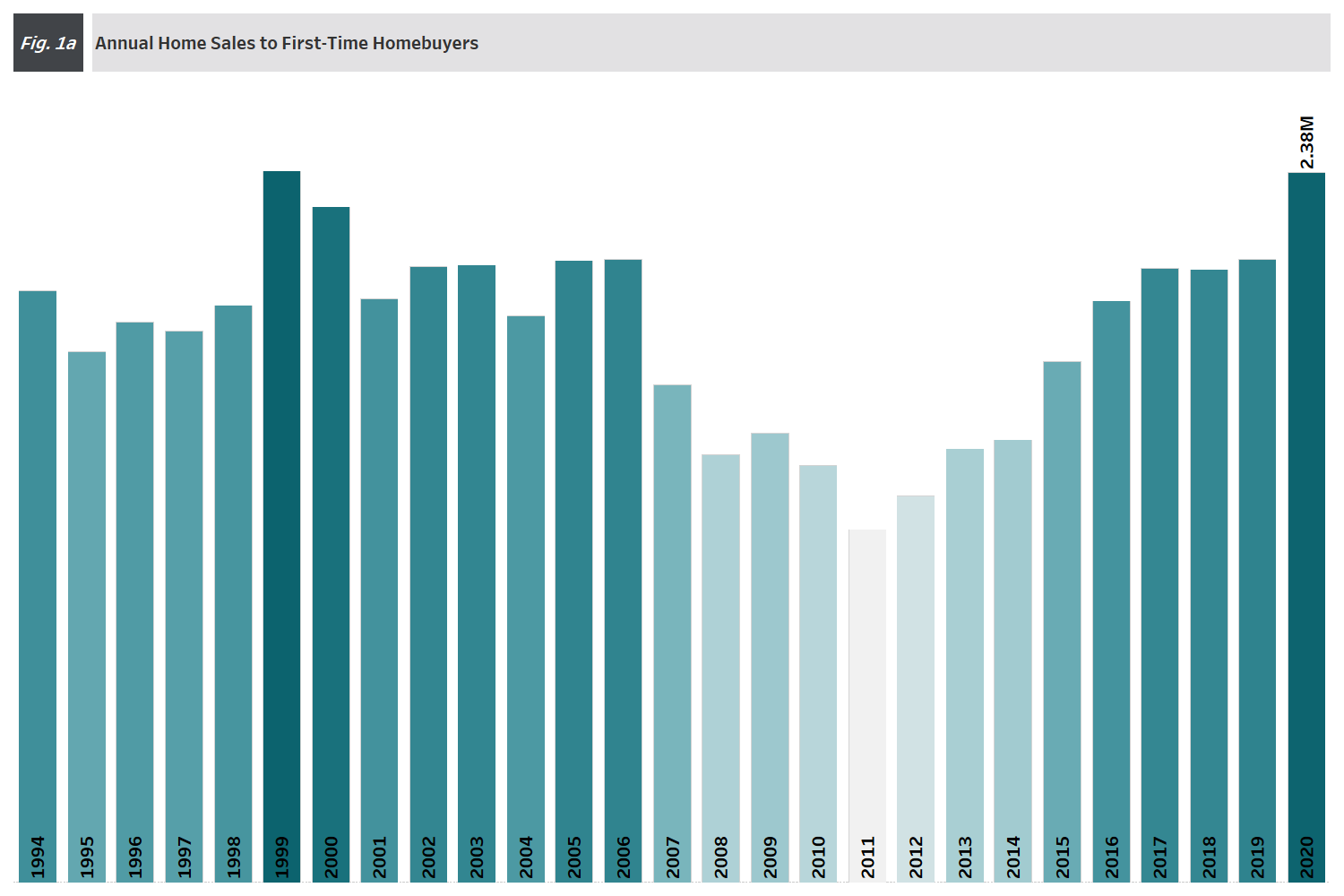

Approximately two million homes are sold to first-time homebuyers every year, according to a report published by Tian Liu, Chief Economist for Enact Mortgage Insurance.

“… there is a strong demographic foundation for this strength, as the largest cohort in history, the Millennial generation, is reaching its early-thirties, their peak homebuying ages.”

In 2020, 2.38 million families in the United States became first-time homebuyers, 14 percent higher than in 2019. “This comes after three years of strong first-time homebuyer market activity, when the number exceeded 2 million each year,” the report says.

The market expects the upside momentum to have continued in 2021, but a slowdown due to rising interest rates in 2022.

But, what is a first-time home buyer loan? It is a mortgage program that focuses on people and families planning to buy their first home. The program combines government assistance with private funding. Furthermore, it covers the collateral elements of a typical mortgage, such as minimal or zero down payments, closing cost waivers, grants, and discount points.

Long story short, first-time home mortgages are loans designed for people who have never owned a home before.

Federal Reserve to increase interest rates three times in 2022 and how does it affect first-time homebuyers

Liu’s report also discusses inflation and interest rates since it claims that lower mortgage rates support housing affordability. “Home prices, down payments, and interest rates all play a role in determining the monthly principal and interest payment, which is one measure of housing affordability relative to a borrower’s income.”

Interest rates on mortgages dropped to the lowest in history between 2019 and early 2021. However, lower interest rates turned up in the last quarter of 2021 and experts predict they will rise in 2022 due to the Federal Reserve’s plans to increase interest rates.

According to Wells Fargo, the Federal Reserve will begin raising interest rates by the second half of 2022; before that, the Fed will end its Quantitative Easing Program by March 2022. Both measures would push up mortgage-related interest rates.

“The Federal Reserve has become increasing concerned about persistently high inflation pressures and, as a result, has initiated and accelerated the tapering of its bond purchases, as well as accelerating its rate hike intentions,” the bank says.

“For the December month, the Fed’s overall bond purchases will amount to $90 billion. Consistent with its December announcement, we forecast the Federal Reserve will lower its bond purchases by $30 billion in each of January, February and March next year, bringing its quantitative easing to end by March 2022.”

The bank states that they “expect the Federal Reserve to begin raising interest rates by the second half of 2022, and we forecast a cumulative 125 bps of rate increase, in increments of 25 bps per quarter, starting in Q3-2022 through until Q3-2023.”

The Fed may also think about March as a good month to hike

That being said, other experts see interest rates hikes as soon as March 2022, pushing housing rates higher sooner than expected.

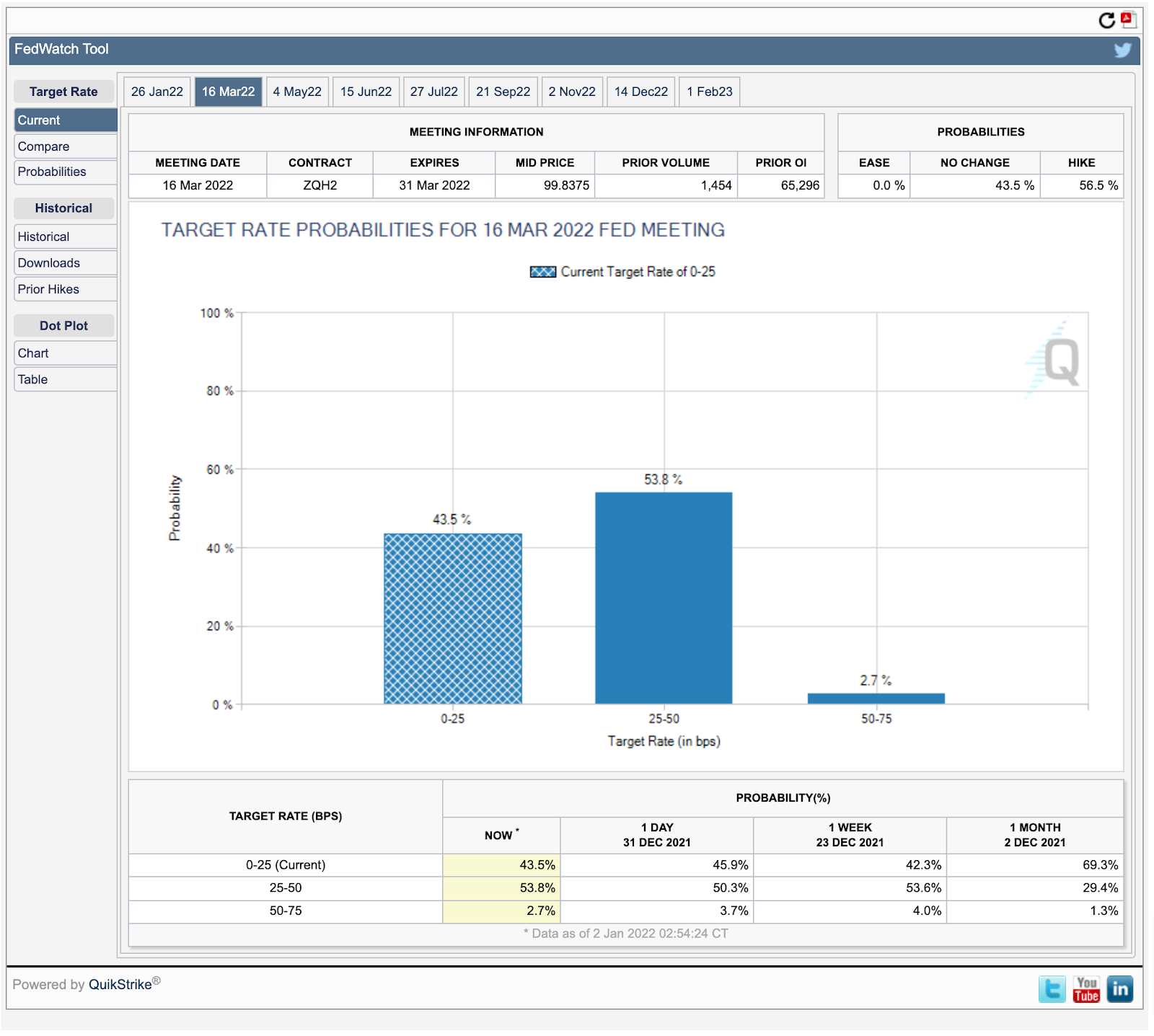

The CME FedWatch Tool, a pool that focuses on target rate probabilities for each Federal Reserve meeting, shows there are 56.5 percent of chances for a rate hike in the March meeting.

What does that mean? First-time home buyers are more aware of increasing interest rates, so they should look for better deals and quick closings before the Fed’s interest rates have a major impact on mortgage rates.

Meanwhile, rising mortgage rates will cool home sales, resulting in a slowdown in the housing market and giving first-time homebuyers extra time to shop houses without worrying about price increases and understanding how much mortgage they can afford.

How does a first-time home buyer loan work?

Mortgages for first-time homebuyers are not strictly different from traditional home loans. The fundamental difference comes with the requirements needed to qualify for the assistance provided by the government and certain private companies.

Companies usually prefer first-time buyers since they will be new customers in the market and turn them into lifelong clients. Furthermore, since they don’t have to sell their property, acquisitions tend to go more smoothly. This is because there is no housing chain in which a home should be sold before purchasing a new one.

As mentioned before, first time home buyer loans have specific requirements. The first criteria is that a person must be a qualified first-time buyer.

Who qualifies as a first-time homebuyer?

- A person who has not owned a principal residence for at least three years

- A single who has only shared ownership with a spouse previously

- An owner of a trailer

- A person who has owned a property that does not comply with building codes

- A single parent who has only owned with his or her ex-spouse while married

Usually, first-time buyers should present proof of income for a minimum of two years, a down-payment of at least 3.5 percent, and a credit score over 620 points.

Some programs allow people to put no down payments and get a mortgage with credit scores as low as 500 if they meet low-income requirements.

Once you meet the requirements, you can explore the different types of loans and mortgages for first time home buyers and choose the best for you.

Tips for First-time home buyers

1. Learn how much mortgage you can afford and be sure you are ready to commit to a loan

When starting your buying process, the most crucial step is to understand your financial limits and possibilities. Be sure you are 100 percent ready to face monthly payments, insurances, property taxes, and regular maintenance of the house.

Mortgage terms vary from person to person, but you can budget accordingly to your finances. It is helpful to have emergency funds that can cover at least three months of expenses and a stable income.

2. Be sure to get pre-approval

People are tempted to skip the mortgage pre-approval process and go straight to house hunting or be confident with a pre-qualification. However, experts do not recommend that. As a second step, it is a very smart idea to get a mortgage pre-approval before starting your search for the appropriate house.

In that way, you will know how much mortgage you can afford and what is your house price range before going wild. It will tell you how much money you have to purchase a house.

Remember that a pre-qualification letter provides you with an estimate of the amount of loan you can get. But not the actual money you would get. It is because pre-qualifications are just an estimate based on informal evaluation of your financials.

On the other side, a pre-approval letter is an official document that a lender will give you with the exact amount of money you will get in your home loan. It is based on reliable information and research done by the lender company. You can count on that money when shopping for your dream house.

With a pre-approval, you will be in a stronger position as a buyer. You will be able to present more solid and stronger offers as the money you show is stable, and at the same time, you will face fewer surprises or even get no loans after making an offer.

3. Boost your credit

One critical step when buying your first house is to build up and improve your credit. Most financial companies prefer credit scores over 700, but 650 is acceptable. Federal programs accept even lower credit scores and poor economic conditions.

Learn how to boost your credit score.

4. Choose the best first time home buyer loan for you

Many people do not get the best deal when purchasing his or her new house just because they do not do their homework. Research for all kinds of types of mortgages and understand your loan options.

If there are multiple types of mortgage loans, why would you want to marry the first one you read about? Do your homework, research and understand every single aspect of the available loans, and choose the best for you.

5. Save for down payment

Down payments are the more significant amount of money you will pay when purchasing a new house. Usually, down payments are at least 3.5 percent of the value of the house. The bigger the down payment is, the better the conditions you will get from your lender.

This is because the lender understands three things with down payments:

- You are also risking your money in the new house.

- They know you control your finances to make savings.

- They will have to lend you less money.

If you can not make any down payment, you may be interested in government-backed programs that offer 100 percent financing on new houses and mortgages with no down payments if you meet the requirements.

6. Remember the closing costs and fees

All mortgages come with closing costs and even some atypical fees from banks or insurances. Keep in mind that the amount of money you will pay goes beyond the house’s value. Typical closing costs vary between two and five percent of total loan costs, and they include:

- Appraisal fees

- Escrow fees

- Title expenses

- Insurance fees

- Attorney fees

- Pest and other inspections

As a first-time buyer, you may qualify for government grants or closing costs free loans.

7. Stick to your budget

Every person wants the best possible house and it usually comes with the mixing of emotions. However, it can cost you money and ugly surprises. Be sure to understand your finances, make your numbers, and shop accordingly.

It doesn’t make sense to look for a house that is 1 million dollars if you can afford a 400 thousand dollar home.

Types of assistance in first-time homebuyer programs

As mentioned earlier, first-time home buyer loans are intended for individuals who are new to the housing market and do not have previous mortgage experience. The programs assist both those with stable financial conditions and those in critical economic situations.

Down payment assistance

Although most people believe they need 20 percent as a down payment to get a loan, many financial companies approve mortgages with as little as 3 percent down. There are other programs that offer first time home buyer loans with zero down. Yes, zero down… no money down.

Down payment assistance for first time home buyers is offered by particular government backed programs. Depending on your situation, down payments can be reduced or assisted, or even considered a grant, which buyers don’t need to repay.

Tax deductions for first time homebuyers

The IRS offers credits for interest rates paid in your mortgage, as well as you can deduct the total amount of your mortgage insurance costs.

First time home buyers can also deduct costs and get tax credits if their property is located in emergency or rural areas. Check your local and state governments for more information.

Closing assistance

As a first time buyer of a house, the government and some private companies offer assistance to reduce the costs of closing your mortgage. Programs include loans to be paid in the term of your mortgage or grants that should not be repaid.

ReadyBuyer

Fannie Mae’s HomePath Ready Buyer program focuses on closing costs for first-time buyers and provides assistance with up to 3 percent of the value of the property on the purchase of a foreclosed property owned by the Federal National Mortgage Association. You should complete a mandatory home-buying educational program to be eligible.

Money from your retirement

All first-time homebuyers are allowed to take up to 10 thousand dollars from his or her Individual Retirement Account, also known as IRA, with no penalty if the reason for the withdrawal is the acquisition of a house. It could be 20 thousand dollars for couples as the limit is per individual.

Additionally, buyers can take the same money from their Roth IRA accounts if they have held the Roth account for at least five years.

Low credit score

Although mortgage programs have a requirement of at least 620 points of credit score, government backed mortgages such as the offered by the Federal Housing Administration accept credit scores as low as 500 points with a 10 percent down payment, or as low as 580 with a 3.5 percent of down payment.

First-time home buyer mortgages programs provided by the federal government

When it comes to talking about mortgages and home loans for first time homebuyers, federal programs are the favorite for people in the United States. Let’s take a look!

Government-backed loans

Among the typical and most popular products with the most affordable conditions for the average American are government-backed and secured loans. With these kinds of programs, you would get low down payments, acceptance even with poor credit scores and lower than average interest rates.

FHA loans, USDA loans and VA loans are three more popular government-backed programs. Please see specific requirements to qualify for one of these and check state and local programs for more options on the Department of Housing and Urban Development (HUD) website.

Good neighbor next door

The Department of Housing and Urban Development offers the Good Neighbor Next Door program, which is a service provided to first respondents, emergency medical technicians, firefighters, teachers, or law enforcement officers to get very affordable properties.

Non-profit first time home buyer programs

The NACA, or Neighborhood Assistance Corporation Of America, is a national non-profit organization that helps people buy a home. The non-profit offers mortgage education for financially unstable households.

They also work like a marketplace where NACA connects low-income people with lenders willing to work with them. They work on personalized paths to get you to homeownership. NACA also helps with no down payment assistance, no minimum credit score, and no closing costs.

Habitat For Humanity

Habitat For Humanity is a popular housing non-profit in the United States. They work with low-income families to get them “simple, decent and affordable” housing options.

How to apply for first time home buyer loan

First-time homebuyers usually should face program requirements. As there are programs for people who are purchasing a new house in most states, the best idea for you is to contact your local office and check your specific requirements and guidelines.

Grants and first-time homebuyer programs provide down payment and closing cost assistance in several ways, including grants, zero interest, and payment plans.

Usually, a minimum down payment is needed and specifics like how long are you planning to live in your house, the area of the property you want to purchase, the work of the candidate, and income limits.

In summary, most programs require:

- Property must be located in the area of application and be a primary residence

- Borrowers must meet income, credit, and price limits requirements

- Home buyer education required

Steps to apply for first time home buyer loans

Understand your economic situation and set financial goals

Before starting the search for your dream house, it is vital to understand your financials and economic situation and your potential income in the short, middle and long term.

The best way to know your numbers is by asking simple questions. How much money do you already have available for down payments? How much money do you own in liabilities? Are you sure you will be able to face monthly payments? How big is your emergency fund?

After understanding your economic situation, you will be able to identify how much mortgage you can afford, what type of house you can purchase and the area you want to live in.

Improve your credit profile

Credit scores are one of the most critical factors determining the conditions you would get in your first-time homebuyer mortgage. As the FHA says on its website, “regardless of the reason, a low credit score can mean a larger down payment requirement or a higher interest rate for a homebuyer.”

It is very important that you work to improve your credit score in that framework. A few points up can be a game changer and save you thousands of dollars. Learn how to improve your credit score now!

Determine how much mortgage you can afford

After understanding your financials and knowing your credit score, it is time to determine how much mortgage you can afford. Perhaps you can get overwhelmed with the total amount of the loan costs, but go easy and identify how much money you are able to pay in monthly payments.

Take into consideration your car loans, liabilities, credit cards, schools you pay for your children, gas, etc. It all counts, and you should be sure you are able to face all of them every month.

Research several first-time home buyer loan programs

As mentioned earlier, there are several programs, grants, and assistance from government and private organizations that want to help you in the acquisition of your first house. Do your homework and research about the conditions offered by federal and state level programs such as the FHA, USDA, VA, etc.

The more you research, the better deals you will identify, the more significant amount of money you will save, and the more beautiful house you will get.

Submit documents

Identify the best programs for you and submit documents either directly to the organization, when it is possible, or go to a lender that supports these programs and submit the documentation. It is important to tell them what you want, and the programs you know are the best for you.

Do not forget to apply for down payment and closing costs assistance.

Shop for a house

After submitting the documents, you will get a preapproval letter with the exact amount of money the lender is willing to give you. With that in hand, go out and start searching for your dream house.

Waiting for the preapproval is always a good idea as you will understand what houses and areas are available for you, and you can focus your efforts on what really works for you. Also, sellers will see you as a solid buyer with an approved mortgage.

Get ready your house for the appraisal

No matter what the seller tells you regarding the price of the house. Go and get your own appraisal. It can be an extra cost, but it is needed. In that way, you will know the actual price of the house, and you will get a report of the house’s condition.

Be sure to get a fully detailed statement about the house you are about to purchase and avoid ugly surprises.

Close the deal in the time of your interest rate lock

After you get the preapproval, you shop the house and make the appraisal, be sure to complete all the paperwork needed for the closing of the home in time to get the sale done.

Finally, be sure you get all the assistance and help provided by first-time buyer programs in your area.

Enjoy your house

You have already purchased your first house. Congratulations! Now it is time to enjoy your home.

What type of loan is best for a first-time home buyer? Pros and Cons

The mortgage market has several options that cover all buyers’ needs, and first-time purchasers are not the exception. For that reason, the best first time home buyer loan for you is the one that solves all your necessities and provides you with the best conditions and the best house in your situation.

Education and research are essential when purchasing a house, but it is mandatory to do your homework and understand the market before you jump in when it comes to first-time buyers.

If you are a low-income individual, you may want to check for government-backed programs and also down payment and closing costs assistance.

However, be sure to understand all the options. Some types of assistance will give you grants, which is like free money, but others will lend you the money for a down payment and you will have to return it later.

Usually, the loans offered by the U.S Department of Agriculture, the Veterans Affairs, and even the FHA are the easiest ones to qualify. But again, it all depends if you meet the requirements.

USDA Benefits:

- No down payment

- No maximum home purchase price

- Interest rates below market averages

- Upfront fees can be added to the total mortgage at closing

- Cheaper monthly mortgage insurance fees

VA loans benefits:

- No down payment

- Low credit scores

- Mortgage rates below market averages

- Accept candidates with bankruptcy and other bad credit information

- No mortgage insurance is required

FHA benefits

- FHA doesn’t lend money, but it secures loans as it provides insurance

- The program insures loans for borrowers with low credit scores

- Down payments as low as 3.5 percent

- Down payment assistance and or gift funds

- A minimum credit score of 500 with a 10 percent down payment, or 580 with a 3.5 percent down payment

- Mortgage insurance premiums can be included in the mortgage

Fannie Mae and Freddie Mac’s Conventional loan 97 benefits

- Down payment of a little as 3 percent

- The mortgage may not exceed $548,250, even if the property is in a high–cost market

- House must be a single–unit dwelling

- No multi-unit homes allowed

- The mortgage must be a fixed-rate mortgage

Know your rights

We will never stress you out enough about research, education, and doing your homework when purchasing your first new home. As you may know, knowledge is power; however, if you get misinformed or feel you have been cheated, be sure there are organizations and government offices that work to defend you.

The Consumer Financial Protection Bureaus is an agency commissioned by the United States government to defend people from companies and to be a vigilant agent in the US housing market.

As their website says, “the Consumer Financial Protection Bureau is a 21st century agency that implements and enforces Federal consumer financial law and ensures that markets for consumer financial products are fair, transparent, and competitive.”

Their mission is “to make consumer financial markets work for consumers, responsible providers, and the overall economy.”

Therefore, if you have any problems, do not hesitate to contact them and expose any doubt or concern you may have. It is important to know your rights, so you should educate yourself, but it is also essential to act if you get into difficulties.