Are you considering refinancing your mortgage? Your new home is already yours after a few years, and you have a better economic status. You might want to reconsider your house monthly payment, or you could try to get a lower interest rate on your home loan after checking what mortgage rates are today.

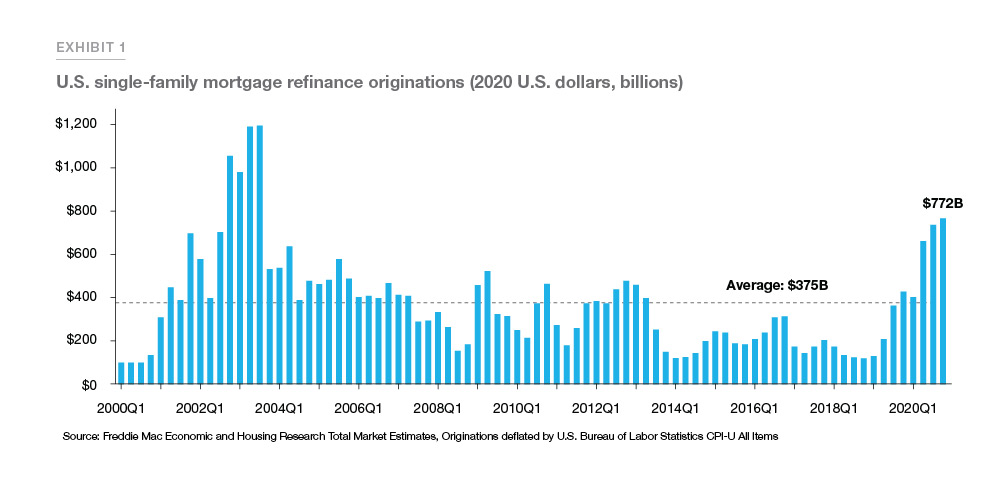

You are not alone, according to a research published by Freddie Mac, refinance originations reached 2.6 trillion dollars in 2020, more than double of refinance originations in 2019 and the highest annual total since 2003.

“There were an estimated $772 billion in inflation- adjusted 2020 dollars in single-family first lien refinances in the fourth quarter 2020. For full-year 2020, there were about $2.6 trillion in inflation-adjusted refinance originations, more than double the volume in the prior year, but still less than the $3.9 trillion in 2003.1”

Do you want to know how do you refinance your mortgage and when is it a good idea? Let’s discuss it today.

You should consider the pros and cons of refinancing a house before you do. You may want to lower your monthly payment or simply shorten the length of your mortgage so you can save money over time, or you may want to cash out on the equity you have earned in paying back your home.

Learn everything you need to know about refinancing your house before you go ahead with the process, as well as what steps are involved in refinancing a mortgage.

What is refinance mortgage?

The refinance of a mortgage occurs when the existing mortgage is replaced with a new loan. Often, homebuyers refinance their houses to lower their payments, reduce the length of their mortgages, stop paying insurances, or take it as an investment with their equity as collateral.

A refinance mortgage is simply getting a new loan to replace the original, in order to take advantage of changing personal economic circumstances or market conditions.

Smart homeowners know that their mortgage could be one of the most important investments in their lives, so they pay attention to every detail involved and take advantage of every opportunity.

One of them is, of course, refinancing the home loan.

Types of refinancing mortgages

Like any other financial product, mortgages and refinance loans have different types to cover all customers’ needs and conditions.

FHA and VA refinance loans:

The Federal Housing Administration, or FHA, and the United States Department of Veterans Affairs, the VA, offer refinance mortgages with more flexible qualifications requirements than conventional loans.

- FHA and VA offer fixed-rate loans

- There are no income or earnings limits

- The maximum loan amounts may vary by county

- Flexible qualification requirements

Fixed-rate refinance mortgage

Refinancing your mortgage at a fixed rate gives you predictable monthly payments. It doesn’t matter how high or low the interest rates are; you will always pay the same.

Refinance mortgages at fixed rates are a good option if you want to keep stable budgets, plan to stay in your home for many years, and believe that interest rates will rise over the next few years.

Adjustable-rate refinance loans:

As the name implies, adjustable-rate loans entail that monthly payments may change periodically. When refinancing to an adjustable-rate mortgage, the loan provides a lower interest rate for an initial payment period, making it more attractive than a fixed-rate mortgage in the short term.

Your interest rate, however, changes periodically as it is based on the financial index associated with your loan and Federal Reserve decisions regarding monetary policy. So, your monthly payment can go lower but also go higher, making your payments more expensive.

Adjustable-rate refinance mortgages usually have an initial period where the rate is fixed. Then, it is followed by a period with a flexible rate that is revised every six months. This kind of refinance home loan works best if you plan to move before the end of the fixed period or if you want initially low monthly payments with no hesitation of what comes after.

Cash-out refinances mortgages:

This product answers to people who want to borrow against their home’s available equity. A cash-out refinance loan pays off your existing home mortgage and provides you with extra money up to the current equity of your house.

Cash-out refinance home loans are available in both fixed-rate mortgages and adjustable-rate loans. It is a good choice if you want to use your house’s equity as collateral for a low-interest loan.

You can also apply for a home equity line of credit, which is often considered a second mortgage. In the case of a fully paid home, you can use your home as collateral for a home equity line of credit.

Are mortgage refinance rates the same as purchase rates?

Most people find that refinancing their mortgage is one of the best ways to save money on their home loans. This is due to the low interest rates currently available.

As Freddie Mac’s Primary Market Mortgage Survey pointed out, “the 30-year fixed rate mortgage rate averaged 3.1% in 2020, a decline of about 90 basis points from a year earlier.”

However, it also highlighted that house prices rose 11.6 percent on a year-over-year basis in the same period.

As a result, while mortgage refinance rates may seem attractive, it’s important to understand all fees involved. In the end, some refinance mortgages result in higher costs than when you buy a new house.

So, the question here is what is best for you? To refinance your house, or to buy a new one?

How do mortgage refinance rates work?

When refinancing a house, you may find that banks show different rates than the ones you get when buying a new one. Why?

Market conditions

Some banks and financial institutions usually add refinance fees. As a sample, Fannie Mae and Freddie Mac started in 2020 a 0.5 percent fee on refinancing mortgages. Freddie Mac called it the Adverse Market Refinance Fee, and it was introduced “as a result of risk management and loss forecasting precipitated by COVID-19 related economic and market uncertainty.”

High volumes

Another factor that drives refinancing prices higher is the volume of applications. As mentioned in the Freddie Mac research, mortgage refinancing has reached highs since 2003. Well, lenders cannot handle all requests, and it ended in the rise of costs and spreads in the business.

Allocations’ capacity

In the same line, as the housing market is booming, due to historic low-interest rates, banks have problems allocating money for refinancing purposes. So, it pushes refinancing prices higher.

Finally, as you may find out, buying a new house is sometimes more accessible and cheaper in terms of financial conditions. It could be a pain in the back to move out of your home, but it could also be the smart move to do. It is up to you!

So, basically, you should understand that:

- Refinancing your house is not free.

- Do not focus only on the interest rate, there are other important factors such as length, personal situation, and goals.

- You can only refinance your mortgage once.

When to refinance a house?

There can be several reasons you might want to refinance your mortgage. As each person is different, their economic situation and goals are too.

Overall, the best time to refinance your mortgage is when your credit score improves or interest rates had dropped below the level when they were when you closed your previous loan. Experts usually say that it makes sense to refinance a home loan when you can cut your interest rates by at least half a percentage point.

When you refinance your mortgage, you can gain an advantage because:

- The ability to reduce your monthly mortgage payment due to a lower interest rate

- When you can cut the term of your mortgage, you can pay your loan faster and pay less in total interest.

- To change your adjustable-rate mortgage to a fixed-rate loan.

- To eliminate mortgage insurances if you have paid more than 20 percent of the value of your house.

- You need cash, and you want to use your house as collateral for a new loan

How to refinance a mortgage?

Like any financial decision, you should do your homework before moving ahead with the refinancing of your home loan. Remember, you can only refinance your home once.

What are the steps involved in refinancing a mortgage?

Understand your economic situation and set financial goals

The best way to start the process of refinancing your house is to understand what is your financial condition. How much monthly payment can you face? What are your priorities? And, how much mortgage can you afford? Do you need extra cash? What is your credit score and history of payments? Finally, be transparent and honest about your finances.

Determine how much home equity you have

Home equity is one of the foundations of the American dream and the creditworthiness of people who live in the United States. It is the value of your home that exceeds the money you still owe in your mortgage. It will allow you to ask for extra cash and get better mortgage refinance rates.

Think in this way, the more equity you have in your house, the less risk your loaner would take with you. So, it will translate into cheaper fees and lower interests.

Research several mortgage lenders

Compare all offers and choose the best for you. The only way to do that is to get quotes from multiple mortgage lenders. Do your homework! Never accept the first deal you are offered before checking with other lenders. Take into consideration all points and discounts you have available.

Submit documents

After finding the right lender, you should submit all the documentation to refinance your house. It may include personal tax returns, bank statements, etc.

Get ready your house for the appraisal

When requesting a refinancing, lenders will typically do a mortgage refinance appraisal to determine the market value of your house. It is essential to make any reparation you may want to do and make your home looks pretty. Also, highlight all the improvements you have made to your house. Communication is fundamental for the appraisal.

Close the deal in the time of your interest rate lock

It is important to understand that rate locks last anywhere from 15 to 60 days. Be sure that you can close the deal once you get an excellent mortgage refinance rate, and do not lose it!

Pros and cons of refinancing home loan

You may be thinking of refinancing your home, are you not? Consider the advantages and disadvantages.

Pros of refinance mortgage

- Lower monthly payments

- Lower interest rates

- Switch from an adjustable to a fixed-rate mortgage

- Reduce the term of your loan

- Take advantage of your home equity to get cash

Cons of refinancing your house

- There will be refinancing fees

- If you do not negotiate for a reduced amount of time, your mortgage term can be reset.

- You will pay more interest if you don’t reduce the length of your mortgage

- Your monthly payment will be higher if you reduce your loan term considerably

- Your home equity will be reduced when you refinance for cash out

Should I refinance my mortgage?

Now for the million-dollar question. Is it worth refinancing my mortgage? The answer lies in you. Understanding your finances and checking on your credit and financial status is the first step. Additionally, it is a good idea to check current interest rates to see if they are lower than the ones you originally obtained.

Lastly, make sure you can afford any payment you intend to make. Change sometimes comes with maladjustment that can mess up your finances. Prior to refinancing your mortgage, make sure everything is under control.