After working hard for a few years, it is time for you to take that critical step in your life and purchase a house. However, what is a mortgage, and how does it work?

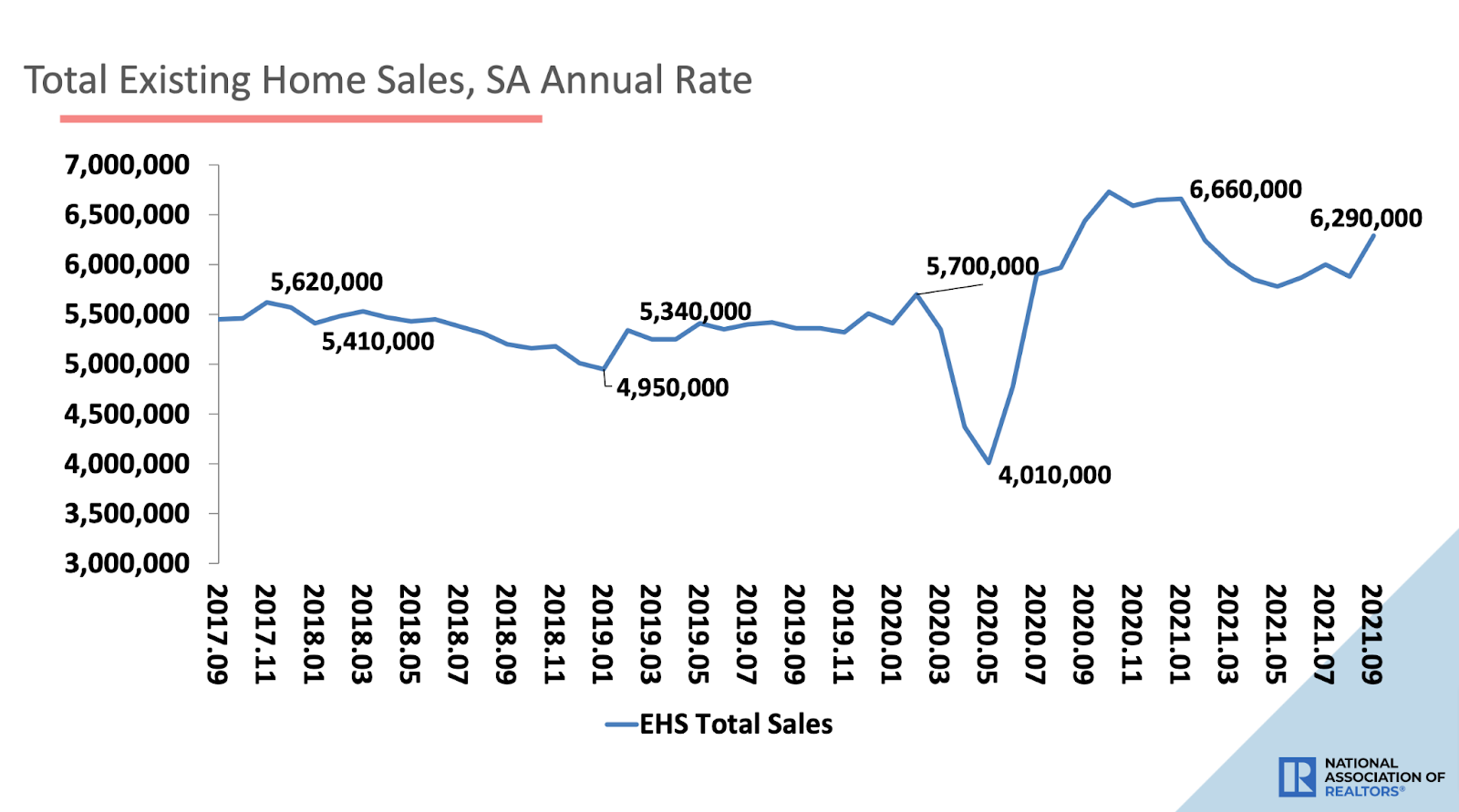

Over 6 million existing houses changed ownership between September 2020 and 2021 at a median price of 352,800 dollars, according to the National Association of Realtors. Despite this, the NAR also reported that the Housing Affordability Index declined from 171.0 in 2020 to 150.9 in September 2021.

Furthermore, NAR reported families are now using 16.6 percent of their income for monthly payments, up from 14.6 percent in 2020. It is interesting that this is happening at a time when interest rates are at record lows, and the effective interest rate on existing-home loans has declined from 3.17 percent in 2020 to 2.95 percent in September 2021, according to the Federal Housing Finance Agency.

These numbers are significant because they will determine your mortgage and what you will pay every month. This will also affect how much mortgage you can afford. Hence, what kind of home you will have.

Housing and work-from-home trends

As you may know, it is essential to consider the type of house you want for living as new job trends suggest remote labor options will push work-from-home positions in the next few years. In fact, according to NAR Chief Economist Lawrence Yun, the outlook for the residential real estate market looks promising.

“We are only in the first innings of work-from-home options,” Yun said. “People have not fully digested the work-from-home-flexibility model yet in determining home size and locational choice.”

Are you ready to expand your options? Read on to learn what’s a mortgage and what topics you should know to get the most competitive deals. We will talk about what a reverse mortgage is, give you a mortgage definition, and how housing loans work.

What is a mortgage in simple words?

Basically, mortgage loans are agreements between two parties where one lends the other money for the purpose of buying a house. As the Consumer Financial Protection Bureau says, “a mortgage is an agreement between you and a lender that gives the lender the right to take your property if you fail to repay the money you’ve borrowed plus interest.”

In plain words, a mortgage is a contract you sign to accept money that facilitates the purchase of a house. Banks, financial institutions, and other mortgage lenders usually offer the cash. The borrower, on the other hand, agrees to pay back the lender usually with recurring monthly payments.

The property itself serves as collateral for the loan. That’s the reason mortgages are considered secure loans.

There are also companies that negotiate with different lenders on your behalf and get you the best deal. These companies are brokers.

What is a mortgage broker, a marketplace and a loan note?

But, what is a mortgage broker? They are usually marketplaces where lenders and borrowers find themselves and, with the help of experts, can match their offerings and needs.

In order to find suitable matches, you must submit documents and obtain mortgage notes and documents.

In another article published here about the story of home-loans, mortgage documents “contains the legal description of the property, details about escrow payment, insurance requirements, liabilities, responsibilities of the borrower, and uniform covenants.”

Now, what is a mortgage note? It is a document that contains the borrower’s promise to pay the lender. “It specifies the loan amount, interest rate, time and place of payments, borrower’s right to repay, loan charges, and what happens when the borrowers miss a required payment.”

Read more about “the origin, story and how does a mortgage work in the success of homebuyers,” and discover how mortgages started as offerings to kings and nobles by 1016 AD, and why all it changed around the 1800s.

Are you a first time home buyer? Read how you can take advantage of your situation and get the best deals from lenders for first-time home buyers.

Types of mortgages

Just as every individual is unique, so are the mortgage offerings. With the evolution of the market from basic money lent to kings and nobles into a multi-cultural and income-transversal sector, the industry developed different types of mortgages to serve different types of borrowers.

Let’s take a look!

Flexible-rate mortgage

Also known as adjustable-rate mortgages or ARMs, flexible rate mortgages work in a mix of adjustable and fixed rates. In general, the first years of your loan follow fixed-rate conditions, while the second part follows flexible conditions based on current interest rates.

As the name implies, adjustable-rate loans entail that the monthly payment may change periodically. When refinancing to an adjustable-rate mortgage, the loan provides a lower interest rate for an initial payment period, making it more attractive than a fixed-rate mortgage in the short term. Read more about adjustable-rate refinance loans.

Fixed-Rate mortgages

Fixed-rate mortgages will work with the same interest rate for the entire life of the loan. People also call them traditional mortgages and are the most popular type of mortgage in the United States. People usually tend to close more mortgages when interest rates are low.

Financing your house at a fixed rate gives you predictable monthly payments. It doesn’t matter how high or low the interest rates are; you will always pay the same.

Interest-only loans

A less common type of mortgage is the interest-only mortgage where you only pay the interest during the first years of the mortgage. So you never touch the principal. People who agree with this kind of deal understand that they will only pay interest, but at the end of the loan, they must return all the money borrowed.

With interest-only loans, home buyers usually don’t build up equity.

Reverse mortgages

When it comes to talking about what is a reverse mortgage, we should refer to a loan that is offered by the equity that you have built up of your house. It is usually used by senior people who are 62 or older who want to have extra cash and don’t worry about the property once they have died.

Usually, reverse mortgages don’t require monthly payments as all the debt will be paid when the borrower dies. According to that line of thinking, relatives would have no rights over the property.

Mortgage refinancing

Despite the fact that it is not a type of mortgage per se, refinancing a mortgage can be considered an option when you want to improve the conditions of your mortgage.

Did you know that “like any other financial product, mortgages and refinance loans have different types to cover all customers’ needs and conditions.”

Who can get a loan?

According to the Mortgage Bankers Association, 1.3 million mortgages were originated in the second quarter of 2021 to purchase a home. Additionally, 1.5 million loans were issued to refinance an existing mortgage. Are you one of those guys? Or did you fail to get mortgage approvals? Let’s see who can get a home loan and how you can achieve success in your endeavor.

So, can anybody get a mortgage? The answer is simply negative. Mortgage lenders usually make decisions on every application depending on different factors such as credit score, history of existing liabilities, and sources of income, among others.

Lenders want to be sure you can pay them back the money, and the risk factors associated with the mortgage should be minimal. Usually, when you look for a loan, it is because you can not pay for the total cost of a house in cash, so you need assistance with the total amount of money.

To qualify for a mortgage, you must meet lenders’ requirements based on your ability to pay back the money and the stability of your income.

Learn how to boost your credit score!

Of course, people who get the best mortgage are those who have the best credit scores, the smaller debt-to-income ratio, and the higher down payments.

On the other hand, there are certain times when people decide to go for a loan despite having the money. It happens with investors who want to use their money in other businesses or people who want to profit from tax credits and fiscal advantages.

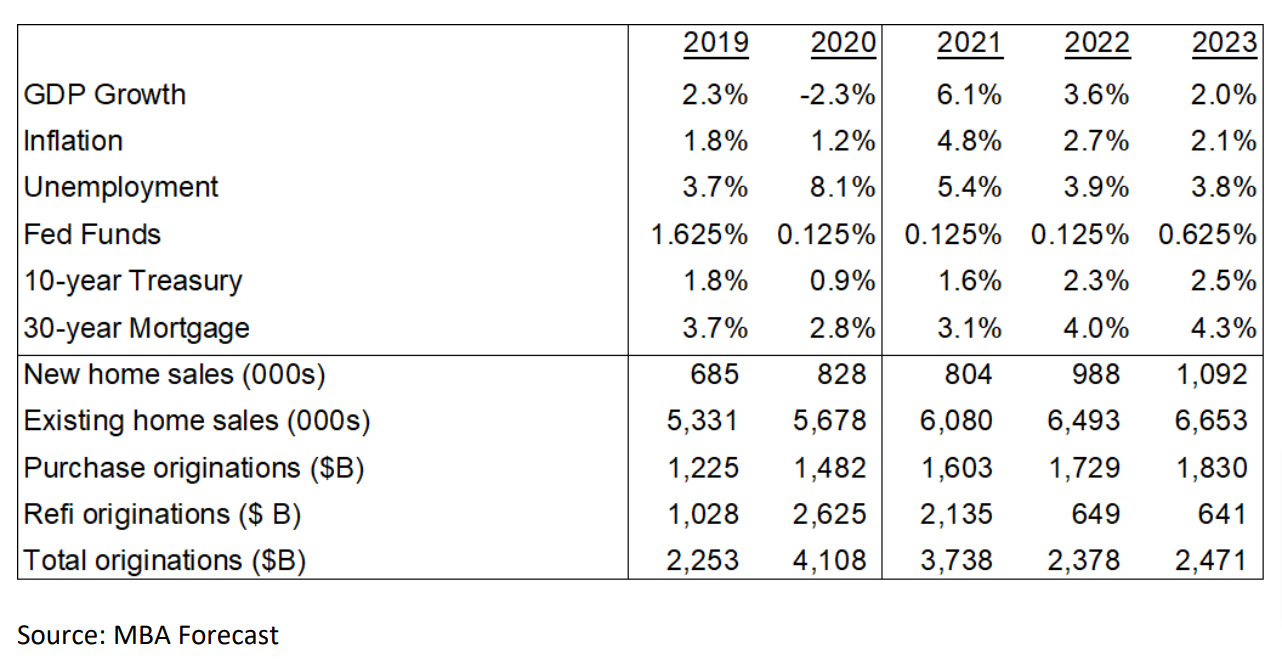

The MBA expects home sales to continue its uptrend in that framework but refinancing to decline due to the Federal Reserve Tapering measures. “MBA is forecasting growth in home sales and purchase mortgage originations for next year and beyond, but does expect a sharp decline in refinance volumes,” The MBA said in its September 2021 Forecast Commentary.

What is the outlook for the mortgage market?

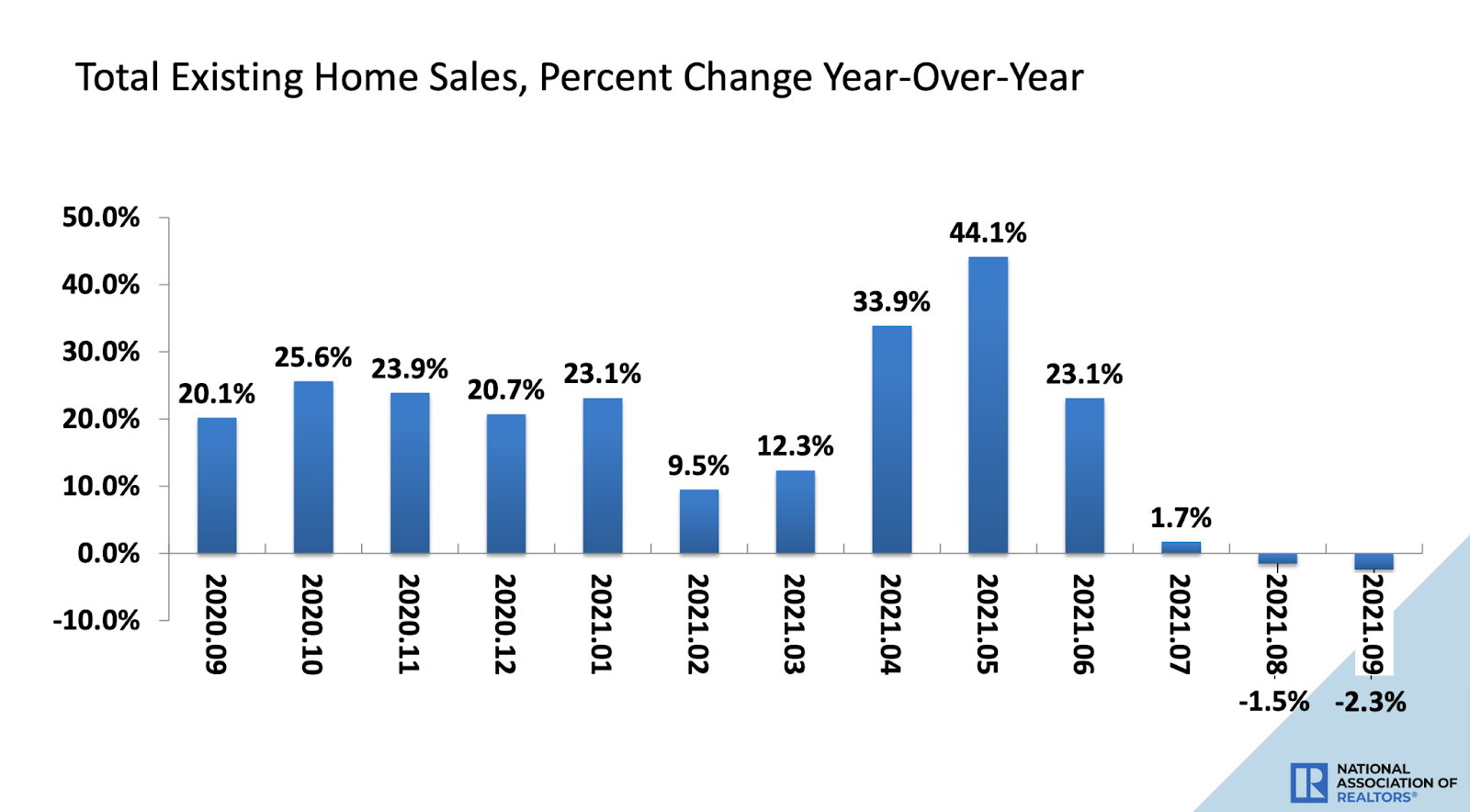

As for now, the housing market is experiencing a slowdown in the inter-annual growth of Total Existing Home Sales with negative numbers in the second half of 2021. Only time will say if we are at the end of the real estate uptrend or not. But in any case, you should be ready to get the best home loans and understand how does a mortgage work.

The MBA considers that the supply chain is becoming a challenge for the real estate market due to disruptions caused by the COVID-19 pandemic. Also, inflation pressures, increasing material prices, and hourly wages push housing prices to the upside.

Experts expect the Federal Reserve to increase interest rates faster than the market previously anticipated. “A first interest rate hike in 2022 and possibly three rate hikes in 2023.”

“Our forecast has the 30‐year mortgage rate is expected to rise to 3.1% by the fourth quarter of this year and to 4.0% by the end of 2022,” the Forecast commentary said. “Originations for 2021 are expected to total $3.74 trillion, with $1.6 trillion in purchase (an 8% increase over the year) and $2.14 trillion in refi (a 19% decrease). For 2022, purchase originations are expected to increase to over $1.7 trillion but refinance volume will decline to $649 billion as rates continue to increase and much fewer refinance candidates are left at those rate levels.”

What makes it difficult to get a mortgage?

When talking about how a mortgage works, we can discuss the specific topics that may prevent you from getting the most favorable deals.

Poor credit score

As with any other financial lending product, mortgages rely upon credit scores to understand the history and quality of the borrower in terms of credits and loans. A FICO score below 620 will put you in a tough position when applying for a conventional loan, while a 580 score is the minimum for an FHA loan.

Check Boost Credit Score, or Establish it in 5 Ways and improve your mortgage options.

A high debt-to-income ratio

Generally, lenders examine your debt to other parties and the amount you owe in relation to your income. As a result, they will be able to assess your financial management skills and the options you have to pay the money back. Look for a debt-to-income ratio of 50% or less.

Interested about how a mortgage can actually improve your credit options? Read Creditworthiness? First-Time Home Buyers Get Houses and understand why home mortgages are considered good loans.

A small down payment

The down payment is seen as a compromise between a buyer and his or her newly purchased home. It is not only that they are reducing the amount of money they are borrowing and, therefore, the amount of interest they pay, but they will also put their own money into the house from day one. As a result, homebuyers will be more inclined to protect their investment. It is recommended to make a down payment of at least 3 percent for some mortgages. However, a 10 percent down payment is considered ideal.

Read How Homeownership Builds Wealth and discover why most experts consider homeownership as the best engine to create long-term wealth.

What are the steps I need to take to determine if I can afford to buy a home and take out a mortgage?

It does not matter what house you want to buy; what really matters is what home you can afford. As mentioned in a previous article, “the most significant factor in a mortgage is whether you can afford it.” Yes, it is true, a mix of fantasy and reality.

“The fantasy is because you have an idealized version of your dream house. On the opposite, dollars and cents determine the reality. You decide to focus on the fantasy house. The mortgage company that is in charge of all the financial details also holds all the cards.”

Now, talking about lenders, they will often tell you how much money you are qualified to borrow. This is, in the same way, how much money they are willing to loan you. In that line, you can check with your bank to have an idea of the size of your budget. However, you can also do your own research.

Doing your homework will help you realize the reality of your finances and improve your numbers. It will even give you tips about preparing your profile as a borrower just ahead of the time you will get into the lender’s office.

Check your liabilities, current monthly payments, how much money your family is doing, and how much money you can pay monthly. Also, take into consideration bonus payments you get so that you can pay the debt down seasonally.

In addition, it is crucial to understand that economic situations change often, and you are not the exception. Consider your risks, way of life, and never stress out your finances too much to get that dream home so that you can be ready in case of difficulties.

Do not overspend!

According to the Consumer Financial Protection Bureau, borrowers should never sacrifice savings in order to buy a bigger house.

“When reviewing your budget to determine an affordable mortgage payment, don’t forget about your savings. You likely will still need to save for emergencies, retirement, college for the children, and other priorities even after you’re a homeowner,” the CFPB said in a 2017 article.

The Consumer Financial Protection Bureau is a U.S. government agency that makes sure banks, lenders, and other financial companies treat borrowers fairly. It also recommends that you should consider adding more money to your emergency fund. The reason is that you should be ready in times of hardships so that you are in the position to avoid going into debt to pay for sudden repairs, replacements, or other necessities.

What to think when purchasing a home and getting a new mortgage

Now that you know what is a mortgage in simple words and how do home loans work, let’s see the CFPB mortgage rules, which are some tips that experienced buyers always point out and the government agency has implemented across the lending market.

“When it comes to shopping for a home mortgage, it should be easy for consumers to find the information they need to make good decisions. The CFPB rules simply require lenders to document a borrower’s ability to repay the loan and follow other common sense rules to protect consumers.”

Only you can decide how much you are comfortable paying for your mortgage.

No matter what a lender tells you. Only you understand your finances and how much you can pay with no problems. Do not lie about your economic situation; lenders have different options for each borrower.

They still have to meet standards and determine if you have the ability to repay your loan, but they can adapt loans to your needs.

Use your market information

As you may know, appraisals provide you with an estimate of what your future home is worth. Be sure you are paying what is fair for the house you are purchasing. Get a copy of any appraisal or valuation a few days before the closing day.

You can also contact an independent appraisal and get a second opinion. Compare prices, and if the assessment is below the price your seller is asking for, you can negotiate with him or her.

“If the appraisal is well below the price you offered to pay, you may want to consider renegotiating the price or reviewing the appraiser’s work carefully to understand how the appraiser arrived at the estimated value,” the CFPB says.

Get experienced help

Always hire experienced and registered people to help you in the mortgage and purchasing process. Ask your loan originator about their credentials, the agency states.

Watch your fees

CFPB mortgage rules limit the fees a lender can impose in a contract. They should follow the requirements as well as you should do too. However, there are certain cases where you will be asked for higher fees. In those situations, check your options and decide what the best way for you is.

As the CFPB says, “be sure to review your closing statement carefully to make sure there are no fees there you did not agree to pay.”

What to look for in a mortgage

A perfect mortgage definition is a contract between you and a lender where the lender gives you money to purchase a house, and you should pay him or her back in a period of time. If you don’t pay the money back, the lender has the right to take your property back. That’s what is a mortgage in simple words.

Can you buy a house without paying mortgage? Of course, you can. But do you have the money for it? Or, what is more interesting… Do you want to buy a house with no mortgage despite all the benefits the U.S. government gives to homebuyers?

Mortgages are considered secured loans because the lender can repossess the property in the case that you fail to pay him or her back. On that edge, what is the difference between a loan and a mortgage?

Well, a loan is an agreement between lenders and borrowers, but the arrangements are not secured, while mortgages are secured loans tied to real estate property. Because, as said before, the property is the collateral and you get the loan against the value of the home you are purchasing, or you already own.

That being said, mortgages have more edges to consider when understanding types, elements and related things.

What you should look for in a mortgage

Down Payment: Determine the money you will pay upfront so you can get better deals and lower monthly payments.

Size of the loan: How much money are you borrowing? Be sure it reflects the amount you need for your house.

Closing costs: Check all fees, costs, and lenders’ fees. Also, watch if there are costs related to any association or local taxes related to your house’s area.

Interest rate: Talk about ways to lower your interest rate and get better deals. Check if your lender institution offers you any discounts or credits.

APR: Check the final Annual Percentage Rate you will pay and if it meets your expectations regarding monthly payments and total interest paid across the life of your mortgage.

Type of interest rates: Check if the lender is offering you a fixed or an adjustable interest and, if it is the case, when does it change so that you can be ready for any eventual change in your monthly payment.

Terms and conditions: Watch out for loan terms, months, any fees for preliminary payments, balloon clauses, interest-only features, negative amortization, or any other clue.

How does a mortgage work

Wise borrowers shop around before applying for a mortgage in a specific financial institution. Remember that you should adapt yourself to the place you are looking for a new house.

Among the factors that affect your mortgage rates, they include the location of the property, your income and liabilities, the size of the down payment, the terms, and type of the loan, as well as your credit score.

Read more about what factors determine your mortgage rates and how to know and take advantage of mortgage rates today.

Once they start the process, lenders will request all documentation. They will check with credit score companies to see if the candidate is suitable to be approved.

As a borrower, you should show proof that you are able to pay back the loan. Documents that will help you on that are:

- Application form

- A copy of your federal tax return

- Wages and tax statements, like a W-2 or 1099

- Recent pay stubs

- Bank statements for your checking and savings accounts

- Statements for investments accounts

- Credit score

- Proof of down payment

- Property appraisal

After reviewing your application, the lender will check your debt-to-income ratio, how good your credit score is and how much you will afford to pay. Therefore, he or she will approve or not your application.

If they approve you, you will get a mortgage note with the amount you have been approved. Then, you can go to the seller and inform him or her you got the money.

Once you get everything right, you should wait for your closing date, which could last around one month while lenders, borrowers and other people involved in the mortgage process do their job.

How to save money on your mortgage

The best way to save on a mortgage is to improve your financial situation before applying for one. By bringing a solid income record, a better credit score, and more money to the lender’s desk, you’ll be able to get a better deal than you could if you had poor financial circumstances.

To save on your mortgage, you should also shop around and visit several banks, financial institutions, and most importantly, the bank where you have your accounts before deciding on a particular mortgage. In most cases, your home bank will offer you discounted points that will lower your interest rate and final APR.

After you have signed your deal, it is advisable to wait a year before considering any changes to your mortgage. Nevertheless, as your economic situation evolves, so should your mortgage.

Refinancing a mortgage is a smart option for improved borrowers. Take advantage of your recently increased credit score, or lower interest rates, and any government assistance you may get.

Are you considering renegotiating your mortgage? In our article, “How to refinance mortgage and when it is a good idea? – The 2022 Guide“, you’ll learn when is the best time to refinance your mortgage and how to get the best deals.

Finally, another option to save money on your mortgage is to make preliminary or seasonal payments. These will lower the interest you will pay during the whole life of the agreement.

Understanding what is a mortgage is the best way to take advantage of your possibilities

Millions of houses change hands every year. The dream of owning a house is achieved by thousands of new homebuyers. There is a saying that the American dream is a big house and a garage for two cars. However, what is the fastest way to get home, and what is the most efficient way to spend your money?

Because we need to be honest. What we really want is to maximize what we can get with our money. Understanding what a mortgage is could help you find a beautiful and comfortable house in the place you want.

Real estate is said to be about location, location, and location. When it comes to buying a house, all you need to know is what your financial options are. Let’s say we have interest rates, a down payment, and discounted points.

By shopping around, you will have more options and will be able to make a more informed decision. Do your homework, and your work will get you a home!